Key Takeaways

AI-powered predictive modeling improves credit risk accuracyEnables faster, automated lending decisionsHelps reduce default rates and financial lossesLeverages diverse data for better risk assessmentEnhances customer experience with quicker approvalsSupports scalable and data-driven financial operations

Predictive Modeling Tools for Credit Risk Analysis: A Practical Guide for Businesses

Predictive modeling tools for credit risk analysis use AI, machine learning, and statistical techniques to analyze historical and real-time data, helping businesses accurately assess borrower risk, reduce defaults, and make faster, data-driven lending decisions.

Modern credit risk analysis is no longer about static scorecards; it’s about dynamic, AI-driven decision-making. Businesses today need predictive modeling tools that go beyond traditional credit scoring systems and leverage machine learning, predictive analytics, and real-time data processing to make smarter financial decisions.

Whether you're a startup fintech company, a large financial institution, or a data-driven enterprise, adopting predictive modeling can significantly improve how you evaluate borrower risk, reduce non-performing assets, and enhance profitability.

Why Predictive Modeling Matters in Credit Risk

Traditional credit risk models rely heavily on historical financial data and predefined rules. While useful, they often fail to capture complex borrower behavior patterns. Predictive modeling changes this by:

- Identifying hidden risk patterns

- Enabling real-time risk assessment

- Reducing manual underwriting efforts

- Improving loan approval accuracy

Key InsightBusinesses using AI-powered predictive models can reduce default rates by up to 20–30% while improving approval speed.

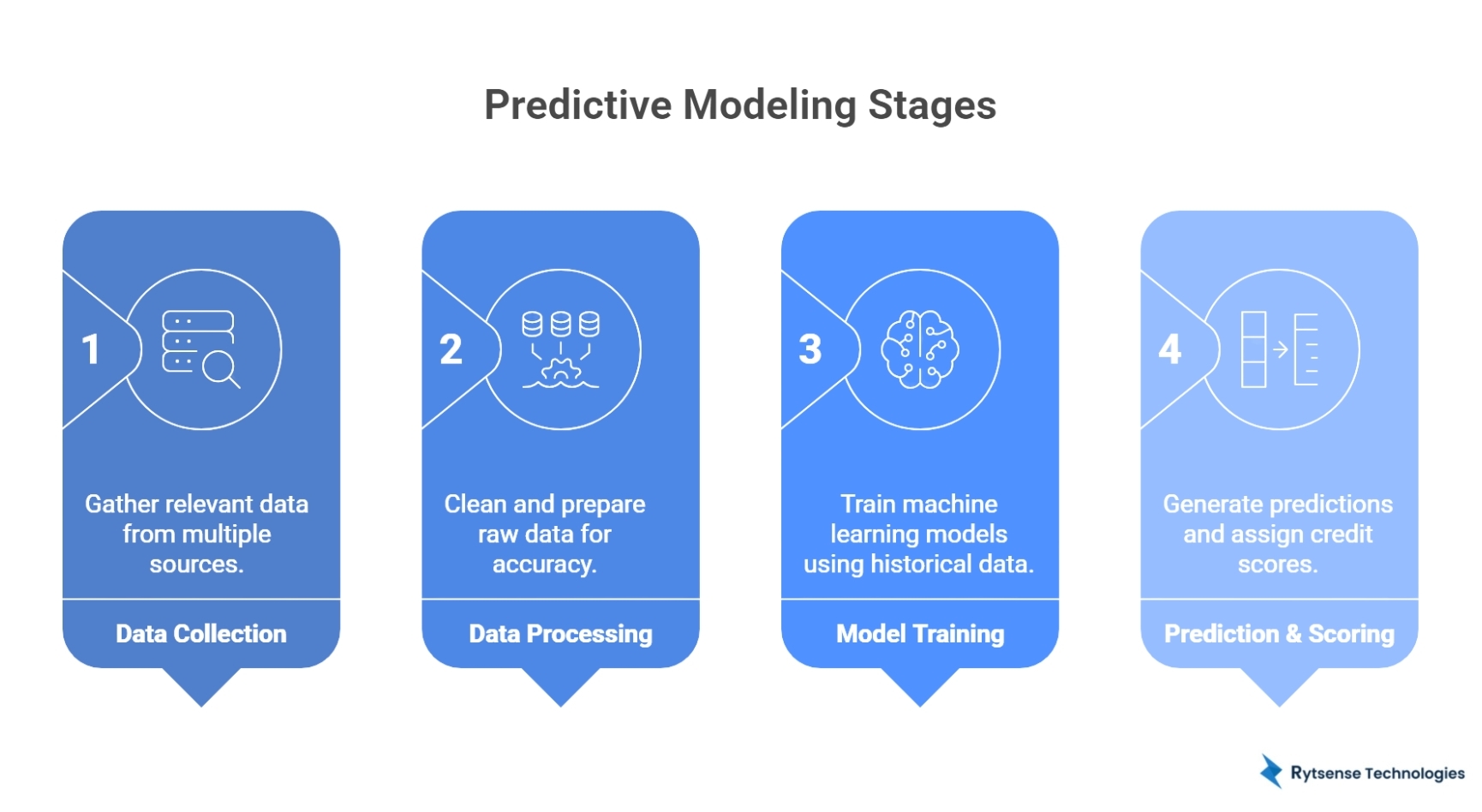

How Predictive Modeling Works

Predictive modeling for credit risk follows a structured process that turns raw data into actionable risk insights. Here's a balanced overview of the key stages:

1. Data Collection

At this stage, relevant data is gathered from multiple sources to build a strong foundation for analysis. This includes:

- Financial history (credit scores, repayment records)

- Transaction data (spending patterns, cash flow)

- Behavioral data (usage patterns, digital interactions)

- Alternative data (mobile usage, social signals, etc.)

2. Data Processing

Raw data is cleaned and prepared to ensure accuracy and consistency. This step typically involves:

- Removing errors and missing values

- Normalizing data for consistency

- Feature engineering to create meaningful variables

- Transforming data into a usable format for models

3. Model Training

Machine learning models are trained using historical data to learn patterns and relationships. During this phase:

- Algorithms identify correlations between borrower behavior and risk

- Models are tested and refined for better accuracy

- The system learns to distinguish between low-risk and high-risk profiles

4. Prediction & Scoring

Once trained, the model is used to generate predictions in real time. It:

- Assigns credit scores or risk probabilities

- Helps in loan approvals, credit limits, and pricing decisions

- Enables faster, data-driven decision-making

Key AI Technologies Behind Credit Risk Modeling

Predictive modeling tools for credit risk rely on a combination of AI technologies that work together to deliver accurate and scalable insights. Here's a clear breakdown:

Machine Learning

Machine learning forms the backbone of credit risk modeling by learning patterns from historical data.

- Supervised learning is used to classify borrowers as low or high risk

- Unsupervised learning helps detect unusual patterns or anomalies that may indicate risk

Natural Language Processing (NLP)

NLP enables systems to analyze unstructured data sources.

- Processes customer documents like loan applications and financial statements

- Extracts useful insights from text data to support decision-making

Deep Learning

Deep learning models handle complex and large-scale datasets effectively.

- Identifies non-linear relationships that traditional models may miss

- Enhances prediction accuracy, especially in high-volume environments

Predictive Analytics

This technology focuses on forecasting future outcomes based on data trends.

- Predicts borrower behavior and repayment likelihood

- Helps identify potential defaults early, allowing proactive risk management

Types of Predictive Models Used

Different predictive models are used in credit risk analysis, each offering a balance between accuracy, interpretability, and scalability. Here's a clear overview:

1. Logistic Regression

A widely used traditional model in credit scoring.

- Simple, fast, and easy to interpret

- Works well for binary classification (e.g., default vs. non-default)

2. Decision Trees

A model that splits data into branches based on conditions.

- Easy to understand and visualize

- Useful for building rule-based credit decision systems

3. Random Forest

An advanced model that combines multiple decision trees.

- Reduces overfitting and improves prediction accuracy

- Handles large datasets with better stability

4. Gradient Boosting (XGBoost, LightGBM)

High-performance models are commonly used in fintech.

- Builds models sequentially to correct errors

- Delivers strong accuracy for complex credit risk scenarios

5. Neural Networks

AI-driven models designed for complex data relationships.

- Handles large and unstructured datasets effectively

- Ideal for advanced, large-scale credit risk applications

Top Predictive Modeling Tools for Credit Risk Analysis

Businesses today rely on a mix of enterprise platforms, open-source frameworks, and cloud-based solutions to build effective credit risk models. Here's a balanced overview of some widely used tools:

1. SAS Credit Scoring

A robust analytics solution designed for financial institutions.

- Offers advanced modeling capabilities and risk assessment tools

- Strong focus on regulatory compliance and governance

2. IBM SPSS Modeler

A popular tool for building predictive models with ease.

- User-friendly interface suitable for both analysts and business users

- Supports a wide range of predictive analytics techniques

3. Python (Scikit-learn, TensorFlow, PyTorch)

A flexible and powerful option for custom model development.

- Highly customizable for advanced machine learning workflows

- Preferred by data science teams for scalability and experimentation

4. RapidMiner

A low-code/no-code platform for quick deployment.

- Enables users to build models without deep programming knowledge

- Ideal for business teams looking for faster implementation

5. H2O.ai

An open-source platform focused on automation and performance.

- Provides AutoML capabilities for faster model development

- Scales well for large datasets and enterprise use cases

6. Microsoft Azure Machine Learning

A cloud-based solution for end-to-end AI development.

- Integrates easily with enterprise systems and data pipelines

- Supports deployment, monitoring, and lifecycle management of models

Key Features to Look for in a Predictive Modeling Tool

When evaluating predictive modeling tools for credit risk analysis, businesses should focus on features that balance accuracy, scalability, and usability. Here's a clear overview:

Accuracy & Performance

The effectiveness of any model depends on how well it predicts risk.

- High precision in identifying low- and high-risk borrowers

- Minimal false positives and false negatives

Scalability

As data grows, your tool should handle increasing complexity.

- Ability to process large datasets efficiently

- Cloud-native architecture for flexible scaling

Explainability

Transparency is critical, especially in financial decision-making.

- Clear reasoning behind model predictions

- Supports regulatory compliance and audit requirements

Integration

The tool should fit seamlessly into your existing ecosystem.

- Easy integration with core banking or financial systems

- APIs for real-time credit scoring and decisioning

Automation

Automation improves speed and reduces manual effort.

- AutoML capabilities for faster model development

- Streamlined workflows from data preparation to deployment

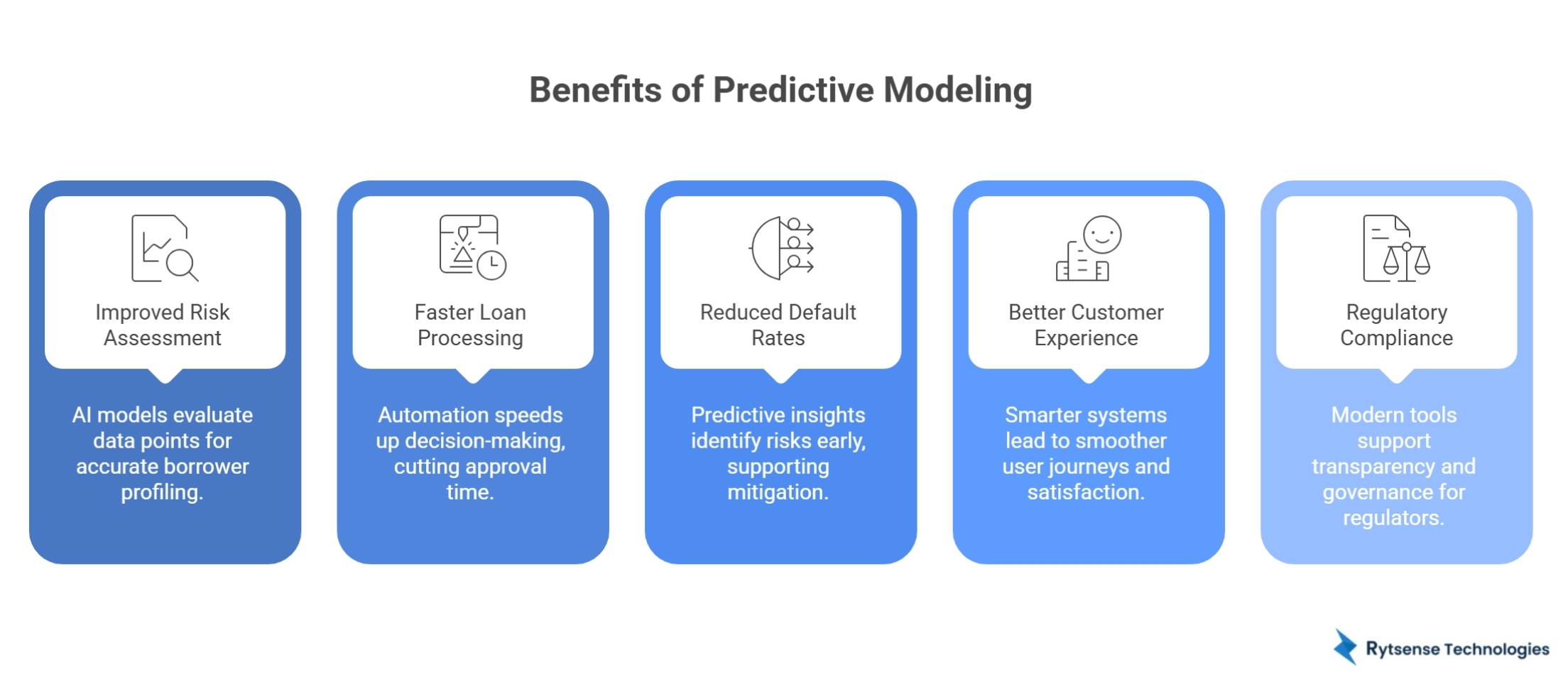

Benefits for Financial Institutions & Fintech Firms

Adopting predictive modeling tools for credit risk analysis delivers measurable advantages across operations, decision-making, and customer experience. Here's a balanced view:

1. Improved Risk Assessment

AI-powered models evaluate multiple data points simultaneously.

- Provides more accurate borrower risk profiling

- Reduces reliance on manual or rule-based assessments

2. Faster Loan Processing

Automation significantly speeds up decision-making.

- Cuts approval time from days to minutes

- Enables real-time credit scoring and instant decisions

3. Reduced Default Rates

Predictive insights help identify potential risks early.

- Flags high-risk applicants before approval

- Supports proactive risk mitigation strategies

4. Better Customer Experience

Smarter systems lead to smoother user journeys.

- Faster approvals improve customer satisfaction

- Personalized loan offers based on risk profiles

5. Regulatory Compliance

Modern tools support transparency and governance.

- Maintain audit trails for every decision

- Provide explainable outputs required by regulators

Challenges and How to Overcome Them

While predictive modeling brings significant advantages, businesses may face a few practical challenges during implementation. Here's how to address them effectively:

Data Quality Issues

Inconsistent or incomplete data can impact model accuracy.

- Solution: Establish strong data governance practices

- Build reliable data cleaning and validation pipelines

Model Bias

Biased data can lead to unfair or inaccurate predictions.

- Solution: Use diverse and representative datasets

- Apply fairness-aware algorithms and regularly audit models

Lack of Expertise

Building and managing AI models requires specialized skills.

- Solution: Hire experienced data scientists or AI engineers

- Partner with a trusted AI development company for guidance

Integration Complexity

Integrating models with existing systems can be challenging.

- Solution: Choose tools with robust APIs and cloud compatibility

- Plan a phased integration to minimize disruption

Real-World Use Cases

Predictive modeling is actively transforming how financial institutions and fintech firms manage credit risk in real-world scenarios. Here are some key applications:

1. Loan Approval Optimization

Predictive models streamline the loan approval process.

- Assess applicant risk quickly using multiple data points

- Enable faster approvals while minimizing default risk

2. Credit Line Management

Credit limits can be adjusted dynamically based on behavior.

- Monitor real-time spending and repayment patterns

- Offer flexible credit limits tailored to individual risk profiles

3. Fraud Detection

AI models help detect unusual or suspicious activities early.

- Identify anomalies in transaction patterns

- Prevent fraud before it escalates into larger losses

4. Customer Segmentation

Borrowers are grouped based on risk and behavior.

- Create targeted financial products and offers

- Improve marketing and risk management strategies

How to Choose the Right Solution

Selecting the right predictive modeling tool depends on your business needs:

For Startups

- Choose low-code platforms

- Focus on quick deployment

For Mid-Sized Businesses

- Use cloud-based AI tools like Azure ML

- Balance cost and scalability

For Enterprises

- Invest in custom AI solutions

- Integrate with existing systems

Future Trends in AI Credit Risk Modeling

Credit risk modeling is rapidly evolving with advancements in AI and data technologies. Here are the key trends shaping the future:

Real-Time Risk Scoring

Credit decisions are becoming faster and more dynamic.

- Enables instant risk assessment using streaming data

- Supports real-time approvals and adaptive credit limits

Alternative Data Usage

Beyond traditional financial data, new data sources are gaining importance.

- Includes social, behavioral, and mobile data

- Helps assess creditworthiness for thin-file or unbanked users

Explainable AI (XAI)

Transparency is becoming essential in AI-driven decisions.

- Provides clear reasoning behind model predictions

- Supports regulatory compliance and builds stakeholder trust

AI-Powered Automation

Automation is streamlining the entire credit lifecycle.

- Enables end-to-end automated credit decision systems

- Reduces manual intervention and operational costs

<a href="https://rytsensetech.com/us/generative-ai-development-services/" class="text-blue-600 underline font-medium">Generative AI</a> in Risk Modeling

A new wave of AI is enhancing predictive capabilities.

- Improves scenario simulation and stress testing

- Helps businesses forecast risks more accurately in changing markets

Conclusion

Predictive modeling tools are transforming how businesses approach credit risk analysis. By leveraging AI, machine learning, and predictive analytics, organizations can make smarter, faster, and more accurate decisions. For financial institutions, fintech firms, and data-driven teams, adopting these tools is no longer optional; it's essential for staying competitive in an increasingly digital financial ecosystem.

Meet the Author

Co-Founder, Rytsense Technologies

Karthik is the Co-Founder of Rytsense Technologies, where he leads cutting-edge projects at the intersection of Data Science and Generative AI. With nearly a decade of hands-on experience in data-driven innovation, he has helped businesses unlock value from complex data through advanced analytics, machine learning, and AI-powered solutions. Currently, his focus is on building next-generation Generative AI applications that are reshaping the way enterprises operate and scale. When not architecting AI systems, Karthik explores the evolving future of technology, where creativity meets intelligence.