Key Takeaways

- AI underwriting in US insurance compresses what once took 2–3 weeks into minutes by automating data ingestion, risk scoring, and decision logic simultaneously.

- Machine learning models now analyze 1,000+ risk variables, from satellite imagery to telematics data, that human underwriters could never process at scale.

- US carriers adopting AI-powered underwriting report loss ratio improvements of 15–40%, making it a direct driver of profitability, not just operational efficiency.

- Straight-through processing (STP) rates above 80% are now achievable for personal lines, freeing underwriters to focus on complex commercial risks that require judgment.

- Regulatory compliance and explainability under NAIC model guidelines and state-level AI rules remain the biggest implementation challenges for US insurers in 2026.

- Carriers that invest in AI underwriting infrastructure now will compound a risk selection and pricing accuracy advantage that competitors cannot easily close.

The US insurance underwriting function is undergoing its most significant transformation in a century. What once required weeks of manual data gathering, actuarial review, and sequential approvals can now be completed in minutes, or even seconds, by AI-powered underwriting systems that are smarter, faster, and more consistent than any human team operating alone.

For insurance executives, underwriters, actuaries, and technology leaders navigating this shift, understanding how AI underwriting works, where it delivers real ROI, and how to implement it responsibly is no longer optional. It is the defining capability question of the decade.

What Is AI Underwriting, and Why Does It Matter Now?

AI underwriting uses machine learning and data analytics to evaluate risk, automate decisions, and price policies faster and more accurately. It matters now because insurers must deliver real-time decisions, improve accuracy, and reduce costs in an increasingly competitive, data-driven market.

Defining AI-Powered Underwriting in Insurance

AI underwriting is the application of machine learning, predictive analytics, natural language processing (NLP), and automated decision engines to assess insurance risk, price policies, and make coverage decisions, tasks that have historically required days of manual review by experienced human underwriters.

In the US insurance market, a $1.4 trillion industry navigating climate volatility, social inflation, and persistent margin compression, the speed and precision of AI underwriting is no longer a competitive luxury. It is a survival imperative.

The Numbers Behind the Urgency

- 90% reduction in underwriting cycle time achieved with full AI automation

- $8.9B projected US AI-in-insurance market size by 2030

- 40% lower loss ratios reported by AI-powered underwriting portfolios

- 3 minutes: average policy decision time for leading AI underwriters in 2026

Why is 2026 a turning point for AI in insurance underwriting?

Three forces are converging simultaneously: the explosion of available risk data (IoT, satellite, telematics, public records), the maturation of large language models capable of processing unstructured documents, and an accelerating underwriting talent gap as a generation of experienced professionals retires. The carriers that automate intelligently now will inherit market share from those that don't.

"AI underwriting is not about replacing actuarial judgment, it's about giving every underwriter the analytical firepower of an entire risk intelligence team, operating in real time."

Why Traditional Underwriting Is Failing the Modern Insurance Market

Traditional underwriting struggles to keep pace with today’s fast-moving, data-driven insurance landscape. Manual processes are slow, inconsistent, and unable to handle the volume and complexity of modern risk signals, leading to delayed decisions and missed opportunities.

The Structural Limits of Manual Risk Assessment

Manual risk assessment relies heavily on static data, human judgment, and fragmented systems, which limits accuracy and scalability. It often overlooks real-time insights, introduces bias or inconsistency, and makes it difficult for insurers to deliver fast, personalized underwriting decisions.

Why is the traditional underwriting process no longer fit for purpose in 2026?

The conventional underwriting workflow was designed for a world of paper applications, static risk categories, and predictable loss patterns. That world no longer exists. Today's risks, cyber threats, wildfire corridors that shift with every drought, pandemic-linked liability, and autonomous vehicle exposure, require dynamic, data-dense risk assessment that human teams alone cannot deliver at scale or speed.

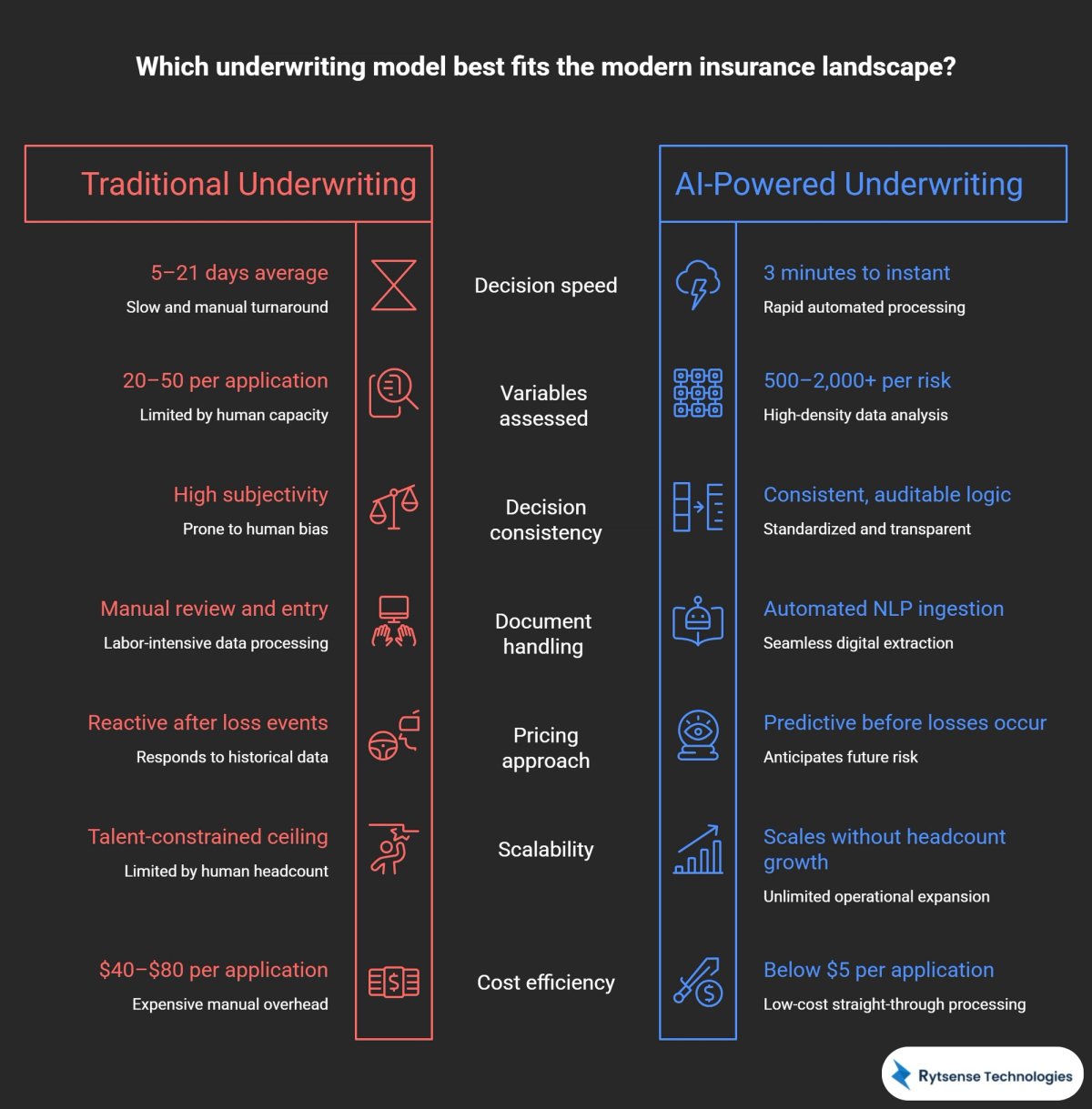

| Dimension | Traditional Underwriting | AI-Powered Underwriting |

|---|---|---|

| Decision speed | 5–21 days average | 3 minutes to instant |

| Variables assessed | 20–50 per application | 500–2,000+ per risk |

| Decision consistency | High subjectivity | Consistent, auditable logic |

| Document handling | Manual review and entry | Automated NLP ingestion |

| Pricing approach | Reactive after loss events | Predictive before losses occur |

| Scalability | Talent-constrained ceiling | Scales without headcount growth |

Beyond speed, the cost gap is widening. Industry benchmarks suggest manual underwriting costs $40–$80 per commercial policy application. AI-driven straight-through processing can bring that below $5 for standard risk profiles, a structural cost advantage that compounds as submission volume grows.

How Does AI Underwriting Actually Work? The Technology Stack

AI underwriting combines data engineering, machine learning models, and real-time decision systems to assess risk faster and more accurately. It transforms raw data into actionable insights, enabling insurers to automate underwriting decisions while improving precision and consistency.

The Five-Stage AI Underwriting Pipeline

AI underwriting typically follows a structured pipeline: data collection from multiple sources, data processing and enrichment, model training and risk scoring, decision-making based on predictive insights, and continuous feedback for model improvement. This end-to-end pipeline ensures scalable, real-time, and data-driven underwriting outcomes.

How does AI make an underwriting decision from start to finish?

Modern AI underwriting operates as a pipeline of interconnected models, each specializing in a stage of the risk assessment process. Here is how a typical submission flows through an AI- powered underwriting system:

Stage 1 : Intake and document processing NLP and large language models extract structured data from unstructured submissions, PDFs, emails, broker notes, loss runs, in seconds, eliminating manual data entry entirely.

Stage 2 : External data enrichment APIs pull third-party risk signals, credit scores, property data, satellite imagery, weather indices, court records, and append them to the risk profile automatically, without underwriter intervention.

Stage 3 : Predictive risk scoring Gradient boosting models (XGBoost, LightGBM) or neural networks score the risk across loss frequency, severity, and correlation dimensions, producing a probability distribution, not a single point estimate.

Stage 4 : Pricing and coverage optimization Actuarial pricing models incorporate the ML risk score alongside market data and reinsurance constraints to generate an optimal premium, deductible structure, and coverage terms.

Stage 5 : Decision and routing Standard risks are approved via straight-through processing (STP). Borderline risks are flagged with AI-generated reasoning and routed to a human underwriter with a pre-built risk summary cutting manual review time by 70%.

Technical note for practitioners: Leading US carriers are now deploying foundation model- based underwriting assistants that allow underwriters to query a risk in natural language "What are the top three loss drivers on this account?" and receive an evidence-backed summary generated from the full submission and portfolio history in real time.

What Data Does AI Use in Insurance Underwriting?

AI underwriting uses a wide range of structured and unstructured data to assess risk more accurately than traditional methods. This includes historical claims data, policyholder demographics, credit and financial information, behavioral patterns, and real-time data from digital interactions and connected devices.

By combining internal records with external data sources, AI can uncover deeper risk insights, detect patterns, and enable more precise, dynamic underwriting decisions tailored to each customer.

New Data Sources Transforming US Insurance Risk Assessment

AI underwriting is expanding beyond traditional datasets by incorporating new, high-frequency data sources that provide deeper and more real-time risk insights. These include telematics from connected vehicles, IoT sensor data from homes and businesses, wearable health data, satellite and geospatial data, social and behavioral signals, and open banking or financial data. By leveraging these diverse data streams, insurers can assess risk more dynamically, improve pricing accuracy, and detect potential issues before they become claims.

What new data sources are transforming insurance risk assessment in the US?

The data revolution in underwriting is as significant as the algorithmic one. AI can ingest and process signal types that were simply impractical for human teams to analyze, unlocking risk dimensions that traditional actuarial models never captured.

- Satellite and aerial imagery : Property condition, roof quality, and wildfire proximity assessed from above with no inspection required. Game-changing for homeowners and commercial property underwriting.

- Telematics and IoT sensors : Real-time driving behavior, commercial fleet data, building sensors, and smart home devices feeding continuous risk signals into dynamic pricing models.

- Alternative credit and financial data : Rent payment history, utility bills, and banking behavior providing a richer financial profile, especially valuable for thin-file or underserved applicants.

- Climate and catastrophe model data : Hyperlocal flood, wildfire, hurricane, and hail risk scores from NOAA, FEMA, and private catastrophe modelers integrated at policy inception, not after binding.

- Legal and court records : Litigation history, OSHA violations, and corporate filings enriching commercial liability and workers' compensation risk assessment automatically.

- Clinical and pharmacy data : With applicant consent, health and life underwriting models use prescription patterns and diagnostic codes to produce more precise mortality and morbidity predictions.

- Conversational and digital signals : Intent signals extracted from chatbot interactions, website behavior, and broker portal activity helping refine risk appetite and customer fit scoring.

"The carriers winning with AI underwriting are not those with the most data, they're those with the best pipelines to turn raw signals into actionable, real-time risk intelligence at the point of submission."

Where Is AI Underwriting Being Applied Across US Insurance Lines?

AI underwriting is being widely adopted across the US insurance industry to improve speed, accuracy, and risk assessment. From personal policies to complex commercial coverage, insurers are using AI to automate decisions, enhance pricing models, and deliver more tailored underwriting outcomes.

AI Underwriting Across Personal Lines, Commercial Lines, and Specialty

In personal lines like auto and home insurance, AI enables instant quotes and usage-based pricing. In commercial lines, it helps assess complex business risks using diverse data sources. For specialty insurance, AI supports underwriting in niche areas such as cyber, marine, and high-value assets, where traditional models often fall short.

Which lines of insurance are seeing the biggest AI underwriting impact in the US?

AI underwriting is reshaping risk assessment across virtually every line of US insurance, though the pace and depth of adoption varies significantly by line complexity, data availability, and regulatory context.

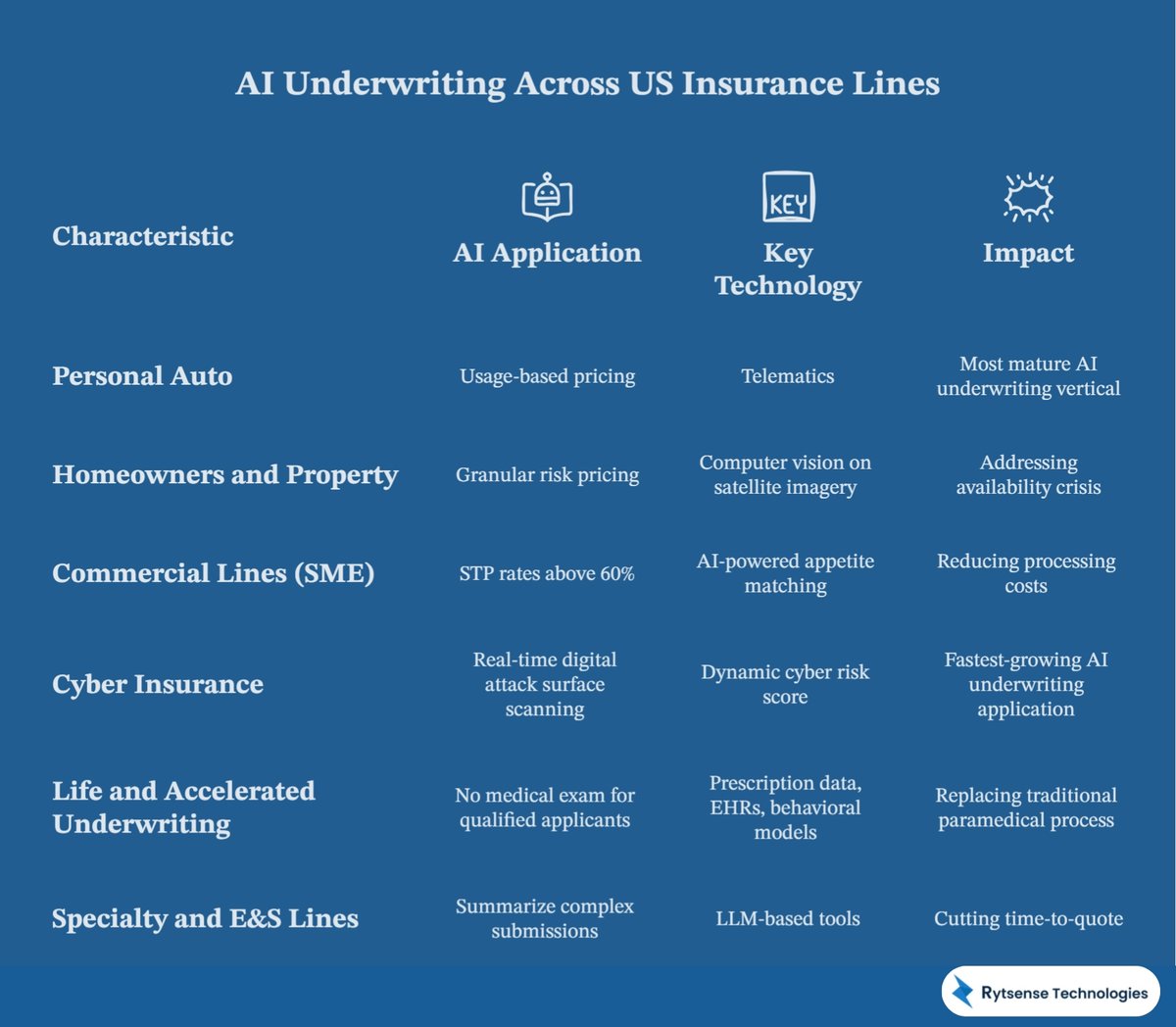

- Personal Auto The most mature AI underwriting vertical in the US. Usage-based insurance (UBI) models from carriers like Progressive and Allstate price dynamically based on telematics. AI-native entrants like Root built their entire model on behavioral data from inception.

- Homeowners and Property AI is directly addressing the US home insurance availability crisis, driven by catastrophic wildfire and hurricane losses, by enabling granular, parcel-level risk pricing that standard actuarial tables cannot achieve. Carriers deploy computer vision models on satellite imagery to assess property risk without human inspection.

- Commercial Lines (SME) Small and mid-market commercial underwriting historically the most expensive to process per submission, is now seeing STP rates above 60% on standard BOP, general liability, and workers' compensation lines, driven by AI-powered appetite matching and automated clearance workflows.

- Cyber Insurance One of the fastest-growing AI underwriting applications. Models now scan the applicant's digital attack surface in real time, open ports, DNS health, dark web exposure, producing a dynamic cyber risk score that updates continuously as the threat landscape evolves.

- Life and Accelerated Underwriting Accelerated underwriting (AUW) programs now approve life policies up to $1–3 million with no medical exam for qualified applicants, using prescription data, electronic health records, and behavioral risk models to replace the traditional paramedical process entirely.

- Specialty and E&S Lines AI is beginning to penetrate the excess and surplus lines market, where complex risks were previously the exclusive domain of senior manual underwriters. LLM- based tools summarize complex submissions and flag key risk factors, dramatically cutting time- to-quote for brokers.

What Are the Business Results? ROI and Performance Metrics

AI underwriting delivers measurable business value by accelerating decision-making, improving risk accuracy, and reducing operational costs. Insurers benefit from faster policy issuance, better loss ratios, increased conversion rates, and enhanced customer satisfaction through more personalized and timely underwriting decisions.

Measurable Impact of AI Underwriting on US Carrier Performance

US insurers using AI underwriting report significant performance gains, including reduced underwriting cycle times, improved pricing precision, lower claims leakage, and higher retention rates. These improvements translate into stronger profitability, scalable operations, and a competitive advantage in a rapidly evolving insurance market.

What measurable ROI are US insurers actually seeing from AI underwriting deployments?

The business case for AI underwriting has moved well beyond pilot programs. Carriers with mature AI deployments are reporting results that are reshaping competitive positioning and investor narratives.

- 85% STP rate achieved : For standard personal lines risks at leading AI-native carriers, requiring zero human touch from submission to policy issuance.

- 70% underwriting cost reduction : Per policy processed when AI automation replaces manual data gathering, clearance, and routing tasks.

- 15–40% loss ratio improvement : Reported by carriers using AI-derived risk scores to tighten portfolio selection and improve pricing accuracy at the individual risk level.

- 4× underwriter capacity : Human underwriters supported by AI tools handle four times the submission volume without quality degradation or decision fatigue.

"The most powerful ROI signal from AI underwriting is not speed, it is portfolio quality. Carriers using AI risk selection are seeing fewer adverse development events and more stable loss trends, which is the real competitive prize."

What does AI underwriting mean for customer experience outcomes?

Instant or same-day policy decisions improve close rates by 20–35% for digital-first distribution channels, where applicant and broker patience is measured in minutes, not business days. Faster decisions also reduce application abandonment rates significantly across personal and small commercial lines.

Who Is Leading AI Underwriting in the US? Key Players

AI underwriting in the US is being driven by a mix of established insurers, digital-first carriers, and innovative InsurTech companies. These players are leveraging advanced analytics, machine learning, and automation to transform underwriting processes, improve risk assessment, and deliver faster, more personalized insurance experiences.

Incumbent Carriers, AI-Native Insurers, and InsurTech Enablers

Traditional carriers are modernizing legacy systems with AI to stay competitive, while AI-native insurers are building fully digital, data-driven underwriting models from the ground up. At the same time, InsurTech enablers are providing specialized AI platforms and tools that help insurers accelerate adoption, enhance decision-making, and scale underwriting capabilities efficiently.

Which US insurers and InsurTech platforms are setting the pace for AI underwriting in 2026?

Incumbent leaders investing at scale Progressive, Travelers, Chubb, Hartford, and Liberty Mutual have invested hundreds of millions collectively in AI underwriting infrastructure, deploying ML pricing models in personal and commercial lines at scale across their full submission volumes.

- AI-native carriers built on data Root Insurance (auto), Kin (home), Pie Insurance (workers'comp), and Openly (home) built AI underwriting into their operating model from day one, using it as both a distribution advantage and a loss selection tool that incumbents are now trying to replicate.

- InsurTech platform enablers Planck, Cytora, EigenRisk, and Federato provide AI underwriting platforms that carriers license, embedding ML risk scoring and workflow automation without the multi-year cost of building proprietary systems from scratch.

- Data and analytics infrastructure providers Verisk, CoreLogic, LexisNexis Risk Solutions, and TransUnion provide the enriched third-party data feeds that power AI underwriting models across the industry, making their data assets a strategic chokepoint in the AI value chain.

What Are the Regulatory and Ethical Challenges?

AI underwriting introduces complex regulatory and ethical considerations as insurers must balance innovation with compliance, transparency, and consumer protection. The use of automated decision-making raises concerns around bias, data privacy, and accountability, making responsible AI practices essential.

Navigating NAIC Guidelines, State Regulations, and Fairness Requirements

Insurers must align AI underwriting models with evolving regulations from bodies like the National Association of Insurance Commissioners (NAIC) and individual state laws. This includes ensuring fairness in pricing, avoiding discriminatory outcomes, maintaining data privacy standards, and providing explainable decisions that regulators and customers can trust.

What regulatory rules currently govern AI underwriting in the United States?

AI underwriting operates in one of the most regulated environments in any industry. In the US, insurance is regulated at the state level, creating a patchwork of 50 regulatory frameworks that AI systems must navigate simultaneously, without the benefit of a single federal standard.

- NAIC Model Bulletin on AI : The National Association of Insurance Commissioners issued its Model Bulletin on the Use of Artificial Intelligence Systems in 2023, requiring carriers to ensure AI models are accurate, reliable, and not unfairly discriminatory.

- California, Colorado, and New York have adopted or are adopting similar state-specific frameworks.

- Proxy discrimination risk : AI models using zip codes, credit scores, or behavioral data can produce outcomes that correlate with protected characteristics (race, religion, national origin) even without using those variables directly. This is the central algorithmic fairness concern regulators are scrutinizing in 2026.

- Explainability and adverse action requirements : Adverse action notices under FCRA and state insurance codes require carriers to explain why a policy was declined or priced higher. Black-box models that cannot produce human-intelligible factor-level explanations are becoming a compliance liability.

- Model validation and governance : Regulators are increasingly requiring formal model risk management (MRM) frameworks, model inventories, and periodic third-party audits for AI underwriting systems, mirroring practices already required in US banking under SR 11-7.

- Data privacy laws : California's CPRA, Illinois BIPA, and emerging state-level AI privacy legislation impose data use and consent requirements that directly affect what signals AI underwriting models can legally ingest and retain.

- Regulatory watch: The NAIC's model bulletin and state-level AI fairness regulations are reshaping what US carriers can automate and how they must document and validate every model in production. Compliance is a design constraint for AI underwriting, not an afterthought to be addressed at audit time.

What Does the Future of AI Underwriting Look Like by 2030?

By 2030, AI underwriting will evolve from rule-based automation to fully intelligent, adaptive systems that continuously learn from real-time data. Insurers will shift from periodic risk assessment to dynamic, always-on underwriting that updates decisions as customer behavior and external conditions change.

From Decision Automation to Continuous Risk Intelligence

The future lies in continuous risk intelligence, where AI models monitor signals in real time, predict risks proactively, and adjust pricing or coverage instantly. This will enable insurers to move from reactive decision-making to proactive risk prevention, delivering smarter policies, better customer experiences, and more resilient insurance portfolios.

How will AI change insurance underwriting over the next five years?

The trajectory of AI underwriting points toward a fundamentally different operating model for US insurers, one where risk assessment is continuous, personalized, and deeply embedded in customers' and businesses' daily operations rather than episodic at policy renewal.

- Continuous underwriting Policies priced dynamically based on real-time risk changes, a fleet's safety record, a building's IoT sensor data, a homeowner's wildfire mitigation steps, rather than locked at annual renewal. The policy becomes a living document, not a static contract.

- Autonomous commercial underwriting Complex SME commercial risks, once requiring senior underwriter review of every submission, will be handled end-to-end by AI systems with human escalation reserved only for genuinely novel or extreme exposures outside the model's training distribution.

- Embedded insurance at point of need AI underwriting embedded directly in purchase workflows, home closings, vehicle purchases, business formation portals, delivering instant coverage with no separate application required. The insurance decision becomes invisible to the customer.

- Parametric and index-linked products AI-designed parametric insurance products that pay automatically when a measurable trigger occurs, hurricane wind speed exceeding a threshold, a drought index value, a grid outage of defined duration, with no claims investigation process at all.

- Privacy-preserving personalization Federated learning and differential privacy techniques will allow powerful risk scoring without centralizing sensitive policyholder data, resolving the tension between AI model accuracy and data privacy requirements at a technical level.

"By 2030, the underwriting function will look less like a decision-making department and more like a continuously learning risk intelligence platform, pricing dynamically, selecting risks predictively, and protecting customers proactively."

A Pragmatic AI Underwriting Roadmap for US Carriers

US insurers should start by building strong data foundations and piloting high-impact AI underwriting use cases. They must then scale with explainable models, regulatory compliance, and seamless integration into underwriting workflows.

How should US insurance carriers begin or accelerate their AI underwriting transformation?

The window for strategic differentiation through AI underwriting is open, but it will not remain open indefinitely as the technology becomes table stakes across the market. Here is a pragmatic roadmap for US carriers at any stage of the AI underwriting journey:

1. Audit your data infrastructure before your algorithms. The single biggest predictor of AI underwriting success is data quality, not model sophistication. Carriers with siloed, inconsistent policy and loss data will build on sand. Data unification and governance is the prerequisite investment that determines everything downstream.

2. Start with the highest-volume, most-structured risks. Personal auto and standard homeowners lines are the ideal first deployments. High submission volume means faster model learning; structured data means faster model development cycles. Win there decisively before tackling commercial complexity.

3. Build for explainability from the architecture stage. Choosing interpretable model frameworks and SHAP-based explanation layers at design time is far cheaper, technically and politically, than retrofitting them after a state regulatory inquiry or adverse action challenge.

4. Invest in the human-AI collaboration model, not replacement. The carriers with the best AI underwriting outcomes are not those replacing underwriters wholesale. They are those augmenting experienced professionals with AI-generated risk summaries, portfolio alerts, and decision support tools, driving faster adoption and better decisions simultaneously.

5. Build a model risk management function proactively. State regulators are moving toward formal AI model oversight requirements modeled on banking's SR 11-7 standard. Carriers with MRM frameworks, model inventories, validation documentation, and testing protocols in place will have a significant compliance head start.

6. Partner strategically with InsurTech platforms to compress timelines. Building AI underwriting from scratch requires ML engineering and data science talent that is both scarce and expensive in the current market. Partnering with established platforms like Planck, Cytora, or Federato can compress years of development into quarters of deployment.

Conclusion

The Competitive Clock Is Already Running on AI Underwriting

The transformation of insurance underwriting from a days-long manual process to a minutes- long AI-driven decision is not a forecast. It is already happening at scale across personal and commercial lines throughout the US market. The performance gap between carriers that have embraced this shift and those still running legacy underwriting workflows is widening with every renewal cycle and every new submission cohort.

The AI underwriting advantage is not simply about operational speed. It is about risk selection quality, loss ratio performance, underwriting capacity, and the broker and customer experience of receiving a fair, fast, and transparent coverage decision. Carriers that invest in these capabilities intelligently, with data quality, explainability, and regulatory compliance built into the foundation from day one, will compound those advantages across their entire book of business for years to come.

The question facing US insurance leaders is not whether AI will transform underwriting. It already is. The question is whether your organization will lead that transformation, or spend the next decade trying to catch up to those that did.

Meet the Author

Co-Founder, Rytsense Technologies

Karthik is the Co-Founder of Rytsense Technologies, where he leads cutting-edge projects at the intersection of Data Science and Generative AI. With nearly a decade of hands-on experience in data-driven innovation, he has helped businesses unlock value from complex data through advanced analytics, machine learning, and AI-powered solutions. Currently, his focus is on building next-generation Generative AI applications that are reshaping the way enterprises operate and scale. When not architecting AI systems, Karthik explores the evolving future of technology, where creativity meets intelligence.